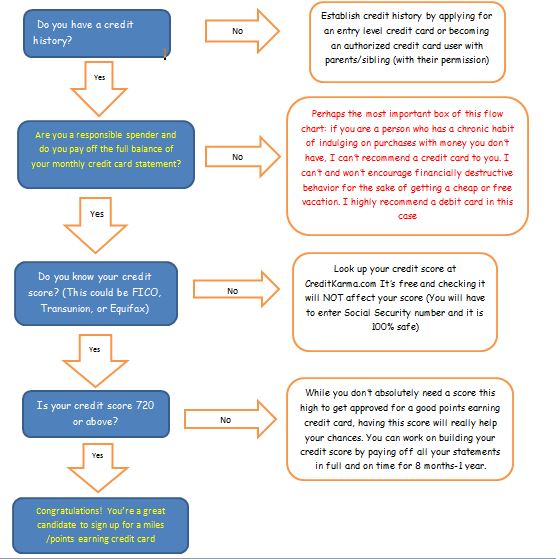

Before getting started on posts detailing the advantages of various credit cards, I wanted to get a few important points across via a simple flow chart. This flow chart is aimed mostly for the younger mid-20’s and under crowd but I suppose anyone can benefit. It is important that you don’t rack up unnecessary spending on a credit card just for the sake of getting the bonus. My general rule is this: If your normal spending habits allow you to get the credit card bonus and you meet the criteria of the flow chart below, go ahead and get it. This includes paying tuition or buying a big ticket item such as a laptop or TV that you would have purchased anyway. If you don’t see yourself spending the $2,000 or $3,000 that is required over the first three months to hit that bonus, wait until an opportunity arises. If you don’t pay off your monthly balance in full, the interest you will pay will negate the benefits you have earned from obtaining the credit card bonus. As the old adage goes, that is like robbing Peter to pay Paul. Credit card bonuses are certainly the easiest way to earn a huge chunk of points/miles but a little discipline is required. If you find yourself not being a good candidate to earn miles via a credit card, don’t be discouraged. There are other ways and I’ll get to those in upcoming posts.

Thanks for reading

– Shiraz